Concentration and Pricing Power: Hospitals versus Insurers

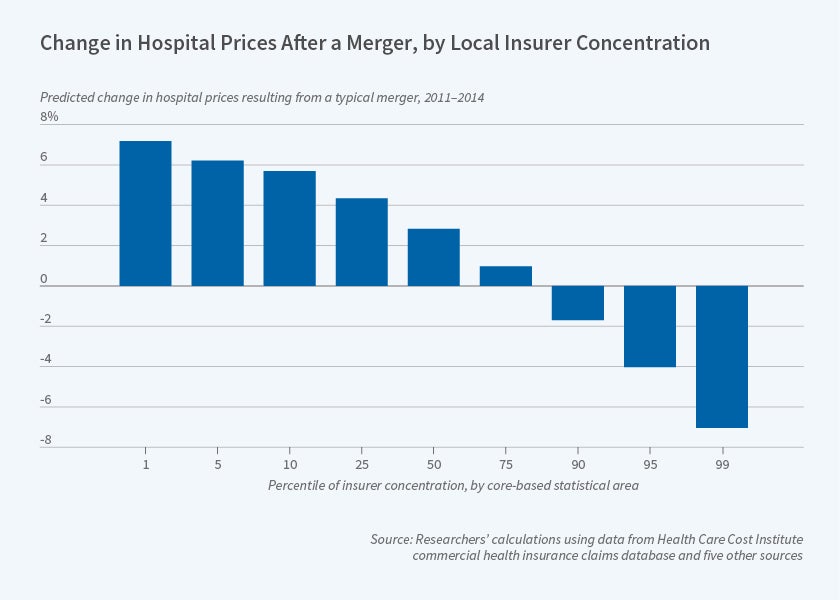

A typical hospital merger would raise the price of an average hospital stay by 4.3 percent in a market at the 25th percentile of insurer concentration, but by only 1 percent in one at the 75th percentile.

The ability of hospitals to raise prices after mergers is significantly blunted in markets with few health insurers, according to findings reported in Countervailing Market Power and Hospital Competition (NBER Working Paper 27005). Eric Barrette, Gautam Gowrisankaran, and Robert Town emphasize that it is essential to consider both the supply- and the demand-side characteristics of a market to make accurate projections of the price impact of potential mergers. They find that a typical hospital merger would raise prices four times as much in a market with many, competitive insurers as in one with a small number of large insurers.

Market power among both sellers (hospitals) and buyers (insurance companies) matters. The most advantageous position for a hospital in terms of maximizing revenue is to be the dominant player in a market with many insurers. It can use its strong bargaining position to command higher prices since insurers must include it in their plans if they are to remain competitive. However, if there are only a few dominant insurers, they can use their monopsony power to drive a better bargain with hospitals.

The researchers study the role of hospital and insurer competition using data on health care claims over the period 2011–14 from three national insurers: Aetna, Humana, and UnitedHealthcare. The dataset includes information on 40 million individuals under age 65 enrolled in employer-sponsored care. The researchers reviewed more than 2.25 million hospital admissions and calculated their average prices after adjusting for severity of condition and hospital characteristics.

The researchers also rank markets by their degree of concentration, from lowest (1st percentile) to highest (99th percentile). In a market with the median level of insurer concentration, a hospital at the 75th percentile of concentration can charge 4.6 percent or $538 more per average procedure than a hospital in a market at the 25th percentile of hospital concentration. However, the ability of hospitals to exercise their market power is sharply reduced when the insurer market is highly concentrated. The difference between hospital prices in markets at the 75th and 25th percentiles of the hospital concentration distribution is 7.1 percent when the concentration of insurers is relatively low (25th percentile), but only 1.5 percent if the concentration of insurance companies is at the 75th percentile.

The researchers point out that differences in insurer concentration matter for the impact of hospital mergers. They estimate that a typical hospital merger would increase the average hospital price by 4.3 percent at the 25th percentile of insurer concentration, but only 1.0 percent at the 75th percentile. For this reason, they conclude that regulatory authorities need to consider insurer concentration when evaluating potential hospital mergers.

—Steve Maas